A bank ABA number, also known as a routing transit number (RTN), plays a crucial role in the financial system by ensuring seamless transactions between banks. Whether you're sending money, receiving direct deposits, or setting up automatic payments, understanding the ABA number is essential for smooth banking operations. In this article, we'll delve deep into what an ABA number is, its functions, and how it works.

As the backbone of the U.S. banking system, ABA numbers ensure that funds are routed to the correct financial institution. These nine-digit codes are assigned to banks and credit unions, making it easier for them to process checks, electronic payments, and wire transfers. Without ABA numbers, the financial system would face significant challenges in ensuring accurate and timely transactions.

This article aims to provide a thorough understanding of bank ABA numbers, including their history, structure, and practical applications. Whether you're a business owner, a student, or simply someone looking to manage your finances better, this guide will equip you with the knowledge you need to navigate the world of banking confidently.

Read also:Unveiling The Ultimate Guide To Football World Cup Venues

Table of Contents:

- What is a Bank ABA Number?

- History and Importance of ABA Numbers

- Structure and Components of an ABA Number

- How to Find Your Bank's ABA Number

- Types of ABA Numbers

- Uses of ABA Numbers

- ABA Number vs. SWIFT Code

- Common Mistakes When Using ABA Numbers

- Security Concerns and Best Practices

- Conclusion and Next Steps

What is a Bank ABA Number?

A bank ABA number, or American Bankers Association routing number, is a unique nine-digit code assigned to financial institutions in the United States. This number identifies the specific bank or credit union involved in a transaction, ensuring that funds are transferred to the correct account. ABA numbers are used primarily for domestic transactions, including check processing, direct deposits, and automatic payments.

The ABA number system was introduced in 1910 by the American Bankers Association to standardize banking processes. Since then, it has become an integral part of the U.S. financial infrastructure, facilitating millions of transactions every day.

Why is the ABA Number Important?

The importance of ABA numbers cannot be overstated. They serve as a digital address for financial institutions, ensuring that funds are routed accurately and efficiently. Without ABA numbers, the banking system would face significant challenges in processing transactions, leading to delays and errors.

History and Importance of ABA Numbers

The history of ABA numbers dates back to the early 20th century when the American Bankers Association sought to streamline banking operations. At the time, the U.S. banking system was fragmented, with no standardized method for routing funds between institutions. The introduction of ABA numbers revolutionized the industry, enabling faster and more accurate transactions.

Today, ABA numbers remain a critical component of the financial system, supporting a wide range of services, including:

Read also:Mt Charleston Weather By Month Your Comprehensive Guide

- Check processing

- Direct deposits

- Automated Clearing House (ACH) transfers

- Bill payments

Structure and Components of an ABA Number

An ABA number consists of nine digits, each with a specific purpose. Here's a breakdown of the structure:

1. First Four Digits: Federal Reserve Routing Symbol

The first four digits of an ABA number represent the Federal Reserve Routing Symbol. This code identifies the Federal Reserve Bank responsible for processing transactions for the financial institution.

2. Next Four Digits: Institution Identifier

The next four digits are unique to each financial institution. These digits identify the specific bank or credit union associated with the ABA number.

3. Last Digit: Check Digit

The final digit is a check digit used to verify the validity of the ABA number. It ensures that the number is accurate and can be used for transactions without errors.

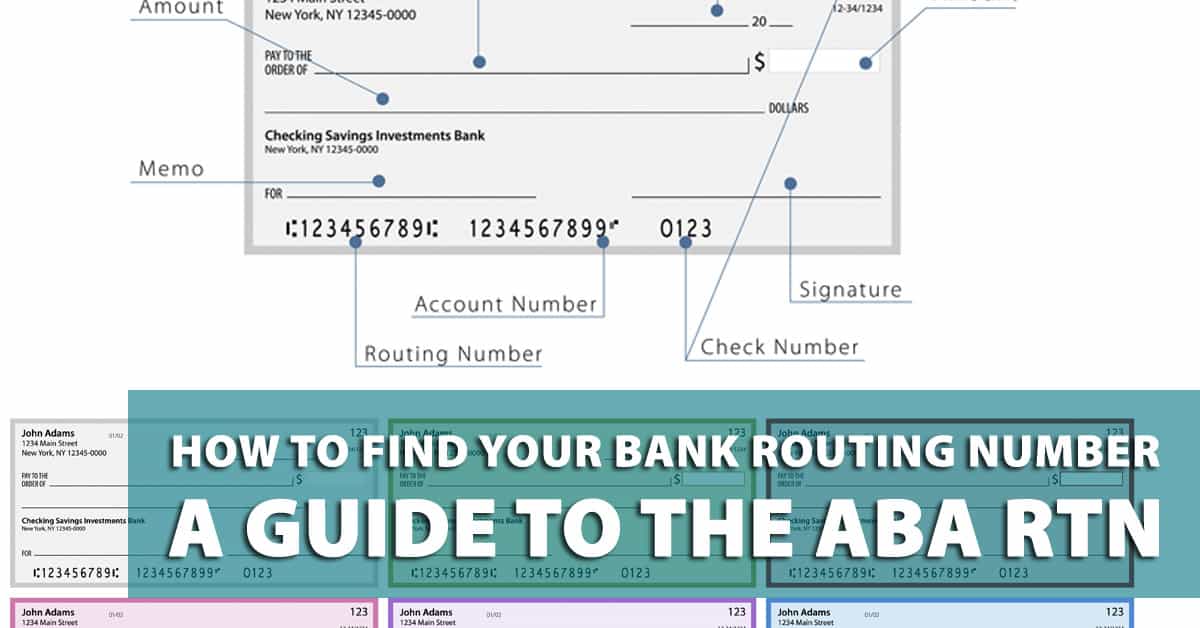

How to Find Your Bank's ABA Number

Finding your bank's ABA number is straightforward. Here are a few methods you can use:

1. Check Your Checks

The ABA number is typically printed on the bottom-left corner of your checks. It appears as a nine-digit code and is usually the first set of numbers in the magnetic ink character recognition (MICR) line.

2. Online Banking

Most banks provide ABA numbers through their online banking portals. Log in to your account and navigate to the account information section to find your ABA number.

3. Contact Customer Service

If you're unable to locate your ABA number, contact your bank's customer service department. They can provide you with the correct number for your account.

Types of ABA Numbers

There are two main types of ABA numbers: ACH routing numbers and wire transfer routing numbers. While both serve similar purposes, they differ in their application:

1. ACH Routing Numbers

ACH routing numbers are used for electronic transactions, such as direct deposits and automatic payments. These numbers are typically the same as the standard ABA number for a bank.

2. Wire Transfer Routing Numbers

Wire transfer routing numbers are used for domestic and international wire transfers. Some banks have separate ABA numbers for wire transfers, so it's important to confirm which number to use for this type of transaction.

Uses of ABA Numbers

ABA numbers are versatile and can be used for a variety of financial transactions, including:

- Direct deposits: Set up automatic deposits for your paycheck, Social Security benefits, or other recurring payments.

- Bill payments: Pay bills automatically using your bank account information.

- Transfers between accounts: Move funds between your own accounts or transfer money to someone else's account.

- Check processing: Ensure checks are processed correctly and funds are deposited into the right account.

ABA Number vs. SWIFT Code

While ABA numbers are used for domestic transactions, SWIFT codes are used for international transfers. Here's a comparison of the two:

ABA Numbers

- Used for domestic transactions within the United States.

- Consist of nine digits.

- Assigned by the American Bankers Association.

SWIFT Codes

- Used for international transactions.

- Consist of eight to eleven characters.

- Assigned by the Society for Worldwide Interbank Financial Telecommunication (SWIFT).

Common Mistakes When Using ABA Numbers

Mistakes when using ABA numbers can lead to delays or failed transactions. Here are some common errors to avoid:

- Using the wrong ABA number for wire transfers or ACH transactions.

- Transposing digits or entering an incorrect number.

- Failing to confirm the ABA number with your bank before initiating a transaction.

Security Concerns and Best Practices

While ABA numbers are essential for banking operations, they can also pose security risks if not handled properly. Here are some best practices to protect your ABA number:

- Keep your ABA number confidential and only share it with trusted parties.

- Verify the recipient's information before initiating a transaction.

- Monitor your account regularly for any unauthorized transactions.

Conclusion and Next Steps

In conclusion, understanding what a bank ABA number is and how it works is crucial for managing your finances effectively. By familiarizing yourself with the structure and uses of ABA numbers, you can ensure smooth and secure transactions. Remember to follow best practices to protect your ABA number and avoid common mistakes.

We invite you to take action by sharing this article with others who may benefit from this information. If you have any questions or comments, feel free to leave them below. Additionally, explore our other articles for more insights into personal finance and banking.

For further reading, consider checking out the following resources:

:max_bytes(150000):strip_icc()/what-is-an-aba-number-and-where-can-i-find-it-315435_final-5b632380c9e77c002c9ef750.png)