ABA numbers play a crucial role in the banking system, ensuring seamless transactions and accurate processing of financial operations. If you've ever wondered what an ABA number is and why it's important, you're in the right place. This article will provide a detailed explanation of ABA numbers, their functions, and how they work in the banking ecosystem.

ABA numbers, also known as routing transit numbers (RTNs), were introduced by the American Bankers Association in 1910 to standardize banking operations across the United States. Since then, they have become an essential component of the financial infrastructure, facilitating smooth transactions between banks and financial institutions.

In this guide, we'll explore the definition, history, and practical applications of ABA numbers. Whether you're a business owner, an individual managing personal finances, or simply curious about banking processes, understanding ABA numbers is vital for anyone involved in financial transactions.

Read also:Paige From Young Sheldon Age A Comprehensive Guide To Her Role And Character

Table of Contents

- What is an ABA Number?

- History of ABA Numbers

- Structure of an ABA Number

- Functions of ABA Numbers

- How ABA Numbers Are Used

- ABA vs. IBAN vs. SWIFT

- ABA Number Security

- Common ABA Number Errors

- Frequently Asked Questions About ABA Numbers

- Conclusion

What is an ABA Number?

An ABA number, or routing transit number (RTN), is a nine-digit code assigned to banks and financial institutions in the United States. This code identifies the specific financial institution responsible for processing a transaction, ensuring that funds are transferred accurately and efficiently.

The ABA number serves as a unique identifier for banks, allowing them to communicate with one another during financial transactions. It is used in various banking operations, including direct deposits, automatic bill payments, wire transfers, and check processing.

Importance of ABA Numbers

- Ensures accurate routing of financial transactions

- Facilitates seamless communication between banks

- Reduces the risk of errors in fund transfers

History of ABA Numbers

The concept of ABA numbers was introduced in 1910 by the American Bankers Association to standardize banking operations across the United States. Before the introduction of ABA numbers, financial transactions were often prone to errors due to the lack of a standardized system.

Over the years, ABA numbers have evolved to accommodate the growing complexity of the banking industry. Today, they are an integral part of the financial infrastructure, supporting billions of transactions annually.

Key Milestones in ABA Number Development

- 1910: Introduction of ABA numbers by the American Bankers Association

- 1940s: Expansion of ABA numbers to include electronic transactions

- 2000s: Integration of ABA numbers into modern banking systems

Structure of an ABA Number

An ABA number consists of nine digits, each with a specific purpose. The structure of an ABA number is as follows:

- First four digits: Identifies the Federal Reserve Routing Symbol

- Next four digits: Identifies the bank or financial institution

- Ninth digit: Check digit used for validation

This standardized format ensures that ABA numbers are unique and easily verifiable, minimizing the risk of errors during transactions.

Read also:How Old Is Doctor Disrespect Unveiling The Age And Journey Of A Gaming Icon

How to Validate an ABA Number

The ninth digit of an ABA number serves as a check digit, allowing banks to verify the authenticity of the number. The validation process involves a mathematical formula that ensures the ABA number is accurate and valid.

Functions of ABA Numbers

ABA numbers perform several critical functions in the banking system. These include:

- Identifying the bank or financial institution involved in a transaction

- Facilitating the routing of financial transactions

- Ensuring accurate processing of checks and electronic payments

Without ABA numbers, the banking system would be prone to errors and inefficiencies, making financial transactions unreliable and cumbersome.

How ABA Numbers Are Used

ABA numbers are used in a variety of financial transactions, including:

Direct Deposits

Employers use ABA numbers to deposit salaries directly into employees' bank accounts, eliminating the need for paper checks.

Automatic Bill Payments

Consumers can set up automatic bill payments using ABA numbers, ensuring timely payment of utilities, loans, and other recurring expenses.

Wire Transfers

ABA numbers are essential for domestic wire transfers, allowing funds to be transferred securely and efficiently between banks.

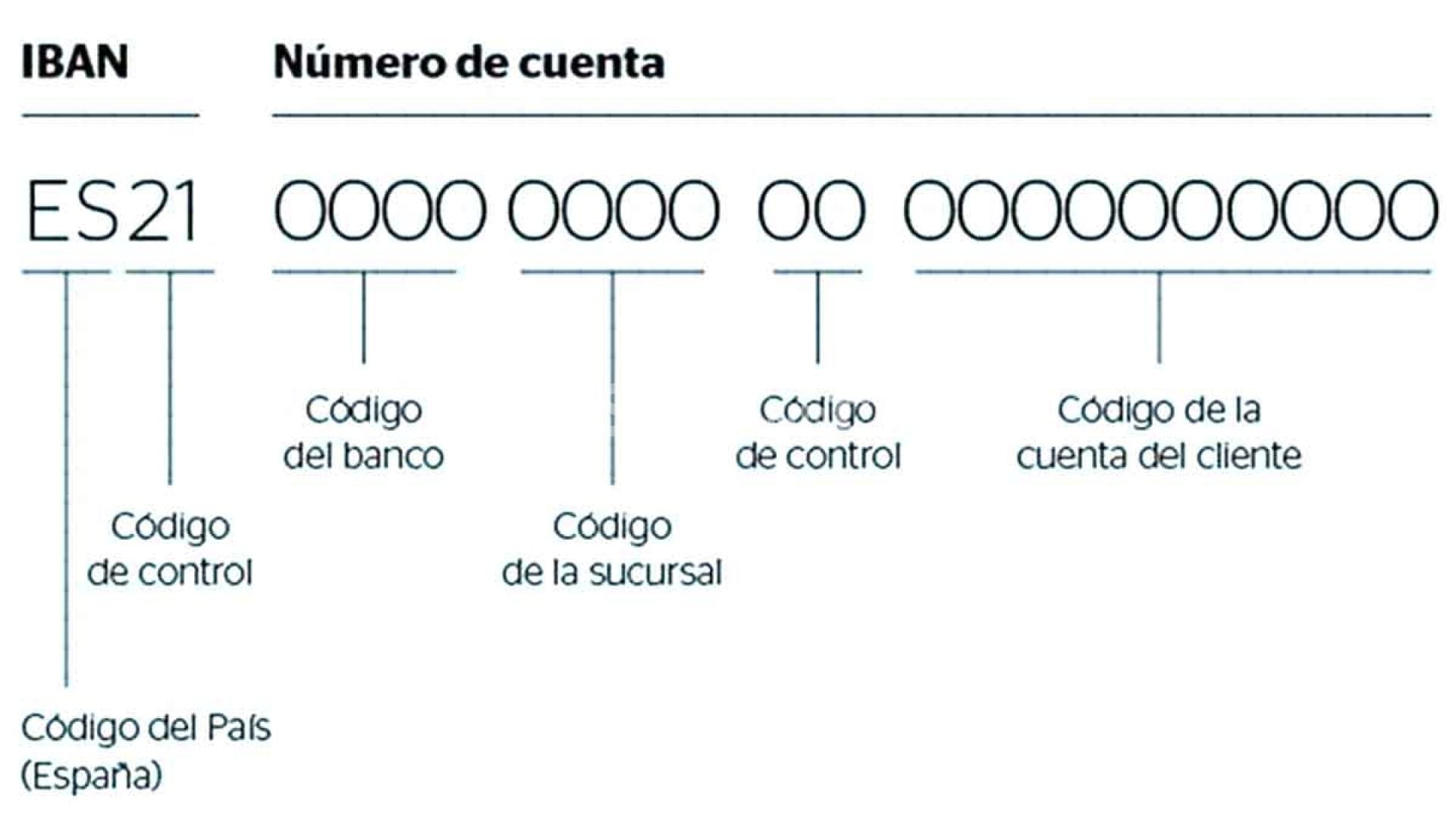

ABA vs. IBAN vs. SWIFT

While ABA numbers are used for domestic transactions within the United States, other systems like IBAN and SWIFT are used for international transactions. Understanding the differences between these systems is crucial for anyone involved in global banking.

- ABA: Used for domestic transactions in the United States

- IBAN: Used for international transactions within the European Union

- SWIFT: Used for international wire transfers globally

ABA Number Security

Security is a top priority in the banking industry, and ABA numbers are no exception. Banks employ various measures to ensure the security of ABA numbers, including encryption, authentication protocols, and fraud detection systems.

Consumers can also take steps to protect their ABA numbers by keeping them confidential and monitoring their accounts for unauthorized transactions.

Common ABA Number Errors

Despite their importance, ABA numbers are sometimes subject to errors. Common mistakes include:

- Transposing digits

- Using outdated or incorrect ABA numbers

- Failing to verify the ABA number before initiating a transaction

To avoid these errors, always double-check the ABA number before initiating a transaction and contact your bank if you're unsure about the correct number.

Frequently Asked Questions About ABA Numbers

Where Can I Find My ABA Number?

Your ABA number can typically be found at the bottom of your checks, on your bank statement, or through your bank's online banking platform.

Can I Use My ABA Number for International Transactions?

No, ABA numbers are only used for domestic transactions within the United States. For international transactions, you'll need to use an IBAN or SWIFT code.

What Happens If I Use the Wrong ABA Number?

Using the wrong ABA number can result in transaction delays, fees, or even the return of funds. Always verify the ABA number before initiating a transaction.

Conclusion

In conclusion, ABA numbers are a vital component of the banking system, ensuring accurate and efficient processing of financial transactions. By understanding the definition, history, and practical applications of ABA numbers, you can better manage your finances and avoid common errors.

We encourage you to share this article with others who may benefit from understanding ABA numbers. If you have any questions or comments, feel free to leave them below. And don't forget to explore our other articles for more insights into the world of finance and banking!

Data Source: Federal Reserve, American Bankers Association